[Addition] Weekly Forecasts 19/2026

Incorporating the effect of China

Yesterday, we published this week’s Weekly Forecasts, which did not make for pleasant reading. I noted in the introduction that

More precisely, even our standard forecasts, assuming no crisis, paint a picture of the global business cycle heading down steeply from henceforth.

This is naturally no surprise, considering the economic hit manifesting from the Middle East, which is now progressing at an increasing speed. Moreover, our oil crisis scenario forecast presents a warning of a collapse of the global economy. It indicates that in just 12 months (this one included), the global downturn would reach the depth of the Great Financial Crisis. I consider this scenario to be worryingly likely.

A thought appeared after their publication.

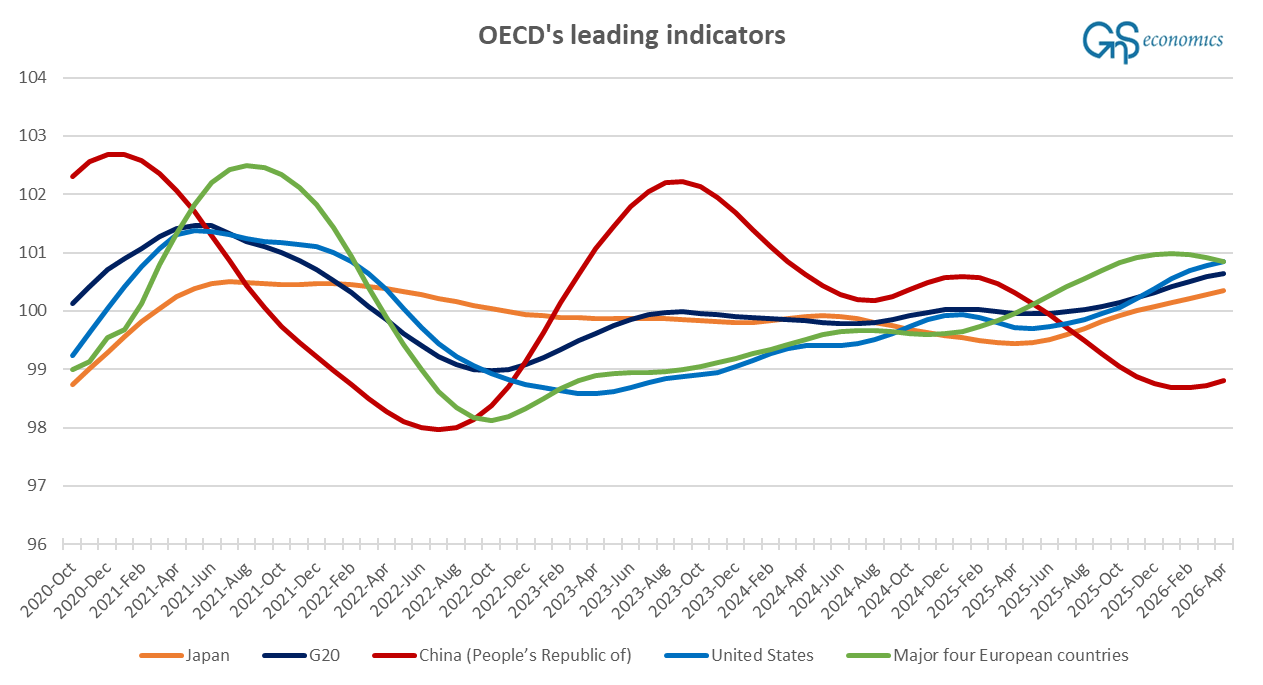

We noted in the free-to-read section that China’s business cycle seems to have bottomed out, driven, most likely, by the strong stimulus push Beijing has run since the start of the year. In terms of OECD’s leading indicators, it looks like this:

There are two main takeaways from the figure above. First is the apparent breaking of the strong upwards momentum of the business cycle of the four major European economies (France, Germany, Italy, and the U.K.). Second is the likely bottoming out of China’s business cycle, as noted above.

I started to ponder, how does the renewed Chinese stimulus and upturn affect the global business cycle?

China was lacking from our forecasts because we needed data going back to the early 1970s to properly model the effect of the first oil shock, whilst China’s data in the OECD’s database range only until early 1992. However, like I have noted also here (see, e.g., this and this), China has been carrying the world economy since 2009. To note, I’ve been a “China bear” since late 2017, but Beijing has surprised me, repeatedly, with their ability to avoid the unavoidable, i.e., the crash of the Chinese economy.

Regardless, the fact that China has (effectively) driven the world economy could affect our forecast on the impending global recession. This is because the effect of the renewed stimulus by Beijing, properly incorporated into our model, could possibly turn the forecast around.

So, what I did is that I ran the forecasts with a shorter time-span with China’s leading indicator included. Figure 2 presents the forecasts for OECD’s leading indicators for China, Japan, and the U.S.1