Weekly Forecasts 21/2026

Forecasting for the continuation of the "bailout" of the U.S. private credit sector

Contents:

Lending to the private credit sector by large U.S. banks accelerates, while lending by small banks stagnates.

Forecasts indicate a steady (rapid) growth of lending to the private credit sector (NDFIs).

(Preliminary) forecasts imply an acceleration of the bailout of Private Credit by large U.S. banks after a brief “summer pause.”

I am glad to start by announcing our traditional summer sale campaign. This year it runs a little over a month until the 30th of June. We offer an annual subscription to our newsletter with 20% off. I urge you to take this offer up, as exciting things are coming for us during the next 12 months. :)

This week, we’ll update the forecasts for lending by U.S. commercial banks and develop something new. By the looks of it, the bailout of the private credit sector, which we speculated to be occurring in early April, is still ongoing, but there’s also something more into it. We suspect that the data center boom has begun to manifest in the bank lending activities of U.S. banks. The question naturally is, for how long does it last?

Our beginning-of-April-forecasts for business lending and lending to non-depository financial institutions by U.S. banks hit their mark well despite some revisions. We continue with the same model, which foresees continued growth of lending.

We also start to experiment with a model predicting the development of NDF lending by small and large U.S. banks. While just a first (preliminary) attempt, the forecasts provide an interesting speculation on the near-future development of bank lending flowing into the private credit sector.

Tuomas

What is happening with U.S. bank lending?

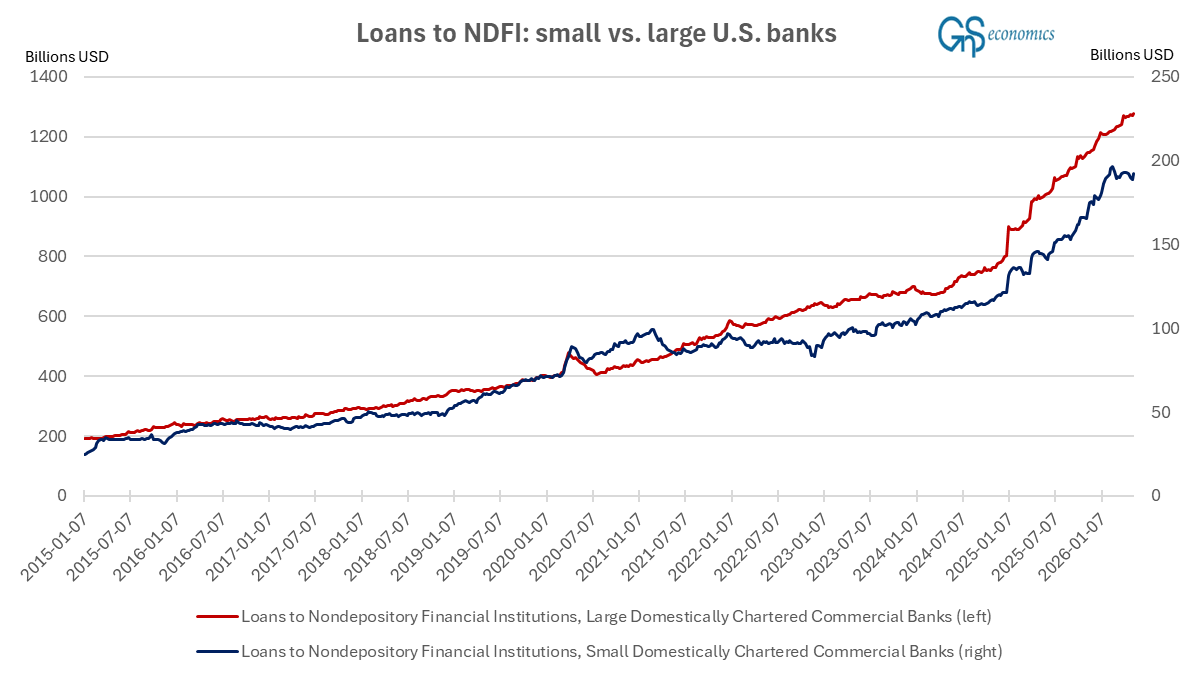

The lending of U.S. commercial banks has continued strong. Figure 1 presents the loans to non-depository financial institutions (NDFIs) from small and large U.S. banks.1

While the large (top 25 by assets) U.S. commercial banks keep pushing money into the NDFIs, small banks continue to shy away. The growth of lending to NDFIs by small banks has stalled in a way we have not seen since 2022. While there have been deeper drops (like in 2025), the ‘stagnation’ of NFDI lending by small banks is starting to become notable, which feeds into our hypothesis of an ongoing bailout of the private credit sector. Because it is mostly the larger banks that are “on the hook” with Private Credit issues emerging there, they should provide most of the “bailout,” while smaller banks would shy away. This is exactly what we are seeing.

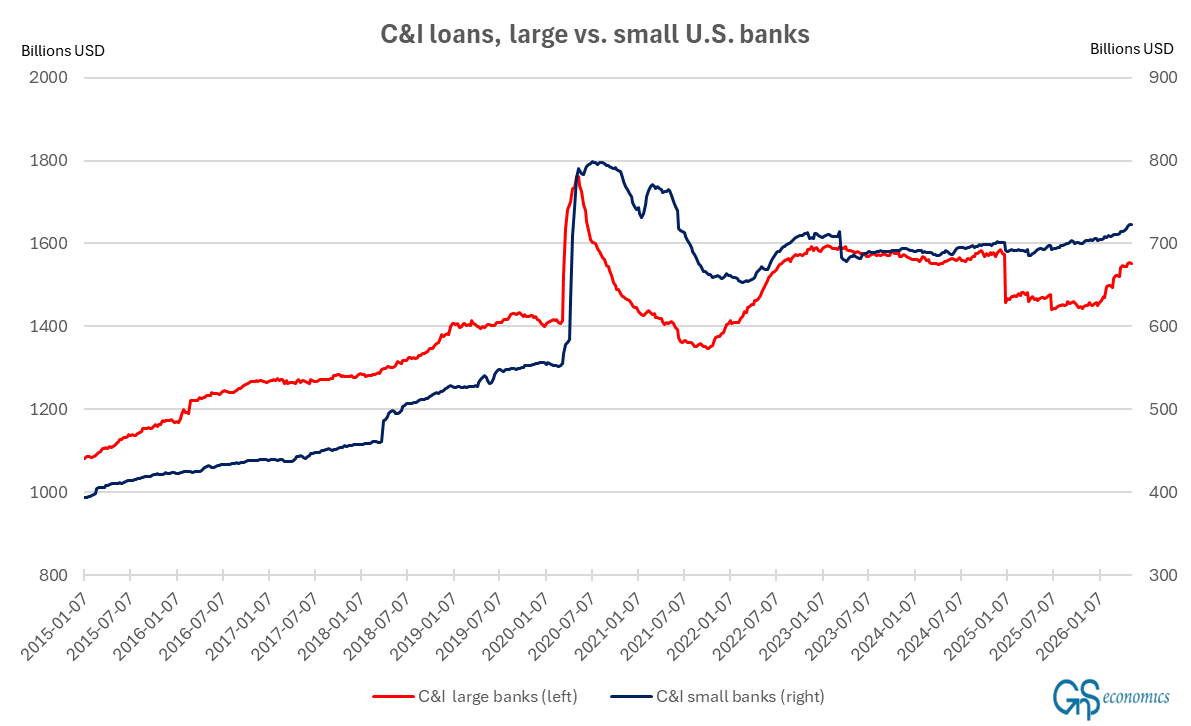

However, there may also be something else going on. Figure 2 presents business (commercial & industrial) loans issued by U.S. banks.

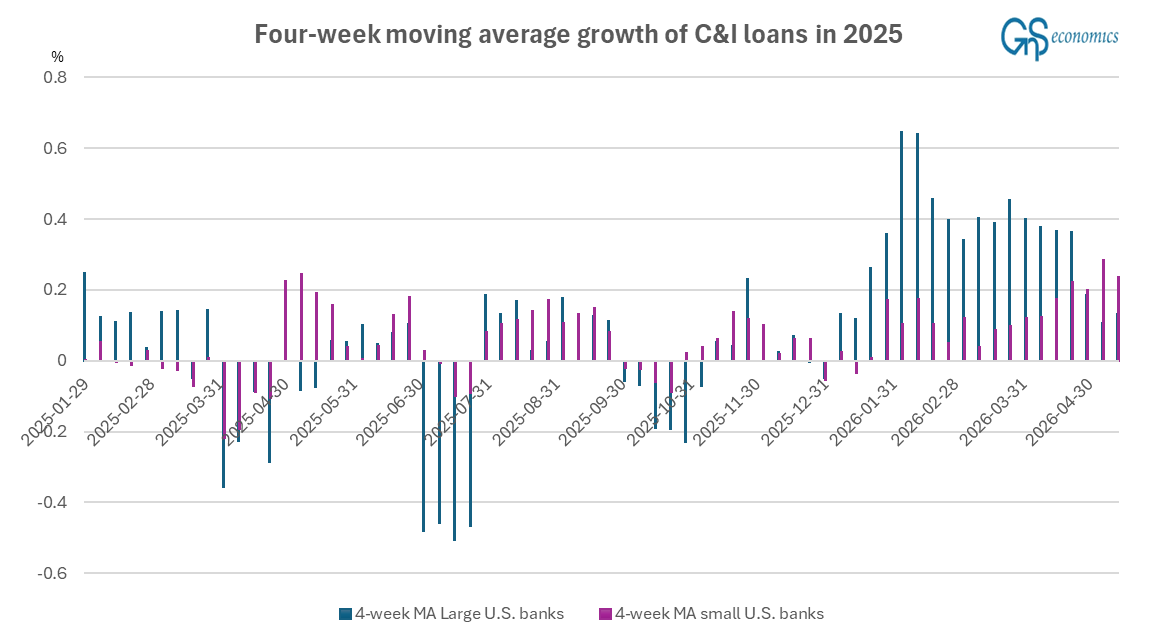

What is now emerging is the growing business lending activity of the small U.S. banks. To emphasize the point, Figure 3 presents the four-week moving average growth of business lending by small and large U.S. commercial banks.

What we observe from the above figure is that in addition to a major increase in the four-week moving average of growth of business lending by large U.S. banks, small banks have also started to increase their lending notably during the past few weeks. This latter part is indicative of growing business activity among small and medium-sized enterprises (SMEs) of the U.S. We consider this to be indicative of the data center boom. For example, Bloomberg noted that data center capital expenditure (CapEx) was close to $750 billion already at the end of March. This is also visible in the U.S. freight, which is growing rapidly currently.

Such developments make it likely that the U.S. economy will not see the plunge our forecasting model has been anticipating since mid-June. Naturally, it would have been impossible for the model to see a major data center boom to manifest during the past few months. That said, we have yet to see the impact of higher gasoline prices and accelerating inflation on the U.S. economy. So, let’s see what comes.

Forecasts for business lending by U.S. banks

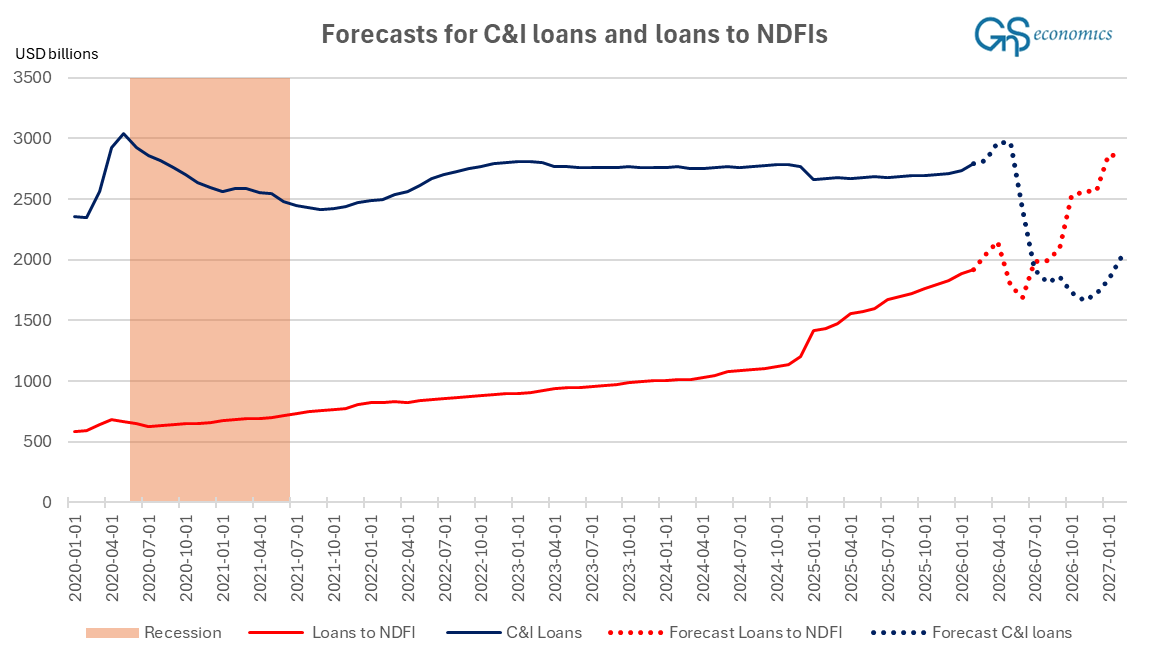

At the beginning of April (with data reaching the end of February), we had two “competing” forecasting models. The one forecasted a gradual increase in lending to NDFIs and business lending, while the other forecasted more drastic movements for the series. The difference between these models was the lag structure. The first one used shorter lags, while the latter had a (much) longer lag structure. Figure 4 presents the latter, i.e., the model that foresaw the drastic developments with a longer lag structure.

We now have a “winner,” and it is not the model that produced the above forecast. Figure 5 presents the forecasts of the former early April model with (smallish) revisions to the data.