Weekly Forecasts 45/2025

The developments in private credit

Bank lending to non-depository financial institutions has accelerated, but there’s more to the story. (Free)

Large U.S. banks are assuming the majority of the risk associated with the private credit sector.

Forecasts indicate that the growth of bank lending to private credit sector will continue unabated.

In my first entry into the series looking at the private credit sector of the U.S. financial system, I noted that:

Private Credit a practice, where private investment funds arrange and originate commercial loans (to businesses). Moreover, loans are not generally traded and are held in majority by the private investment fund (or companies) issuing them.

This sector has been growing rapidly during the past few years, but especially during the past year.

This week we take a deeper dive into the Private Credit through data. We detailed some of the growth of the sector in our October Black Swan Outlook, and now we continue to deepen our statistical understanding of it.

There are two main findings. First, major U.S. lenders are accumulating most of the risk of lending to non-depository financial institutions (NFDI), which includes the private credit sector. Secondly, there are spurts in lending to NFDIs matched by declines in commercial and industrial loans. This indicates that, especially during this year, large U.S. banks have, at times, aggressively transferred their business lending, and the risk associated with those loans, to the “shadow business lending” sector.

Tuomas

Bank lending to the NDFIs

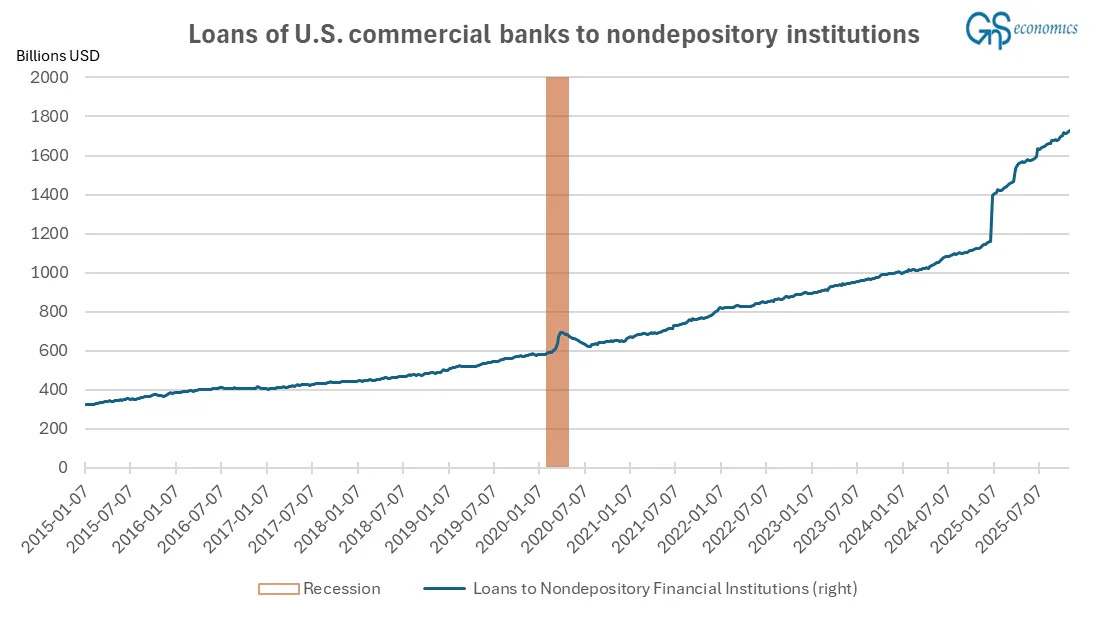

Several exceptional features exist in the development of bank lending to non-depository financial institutions (NDFIs) in the U.S. The first feature is the significant increase observed in the lending series during the first week of 2025. Lending has also clearly accelerated since the start of the year.

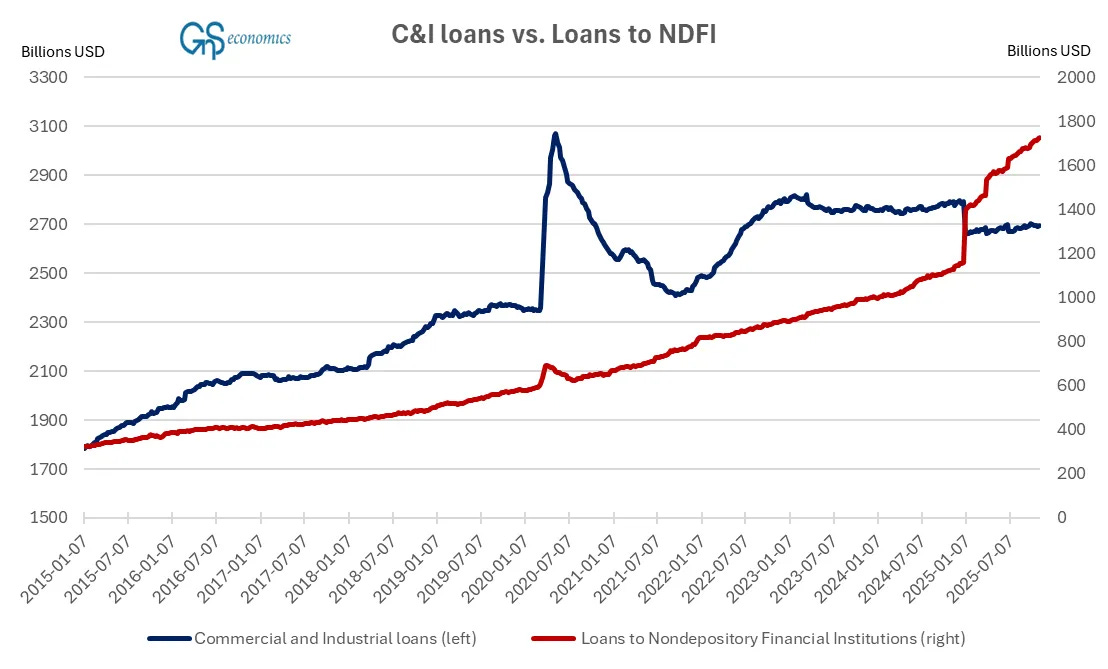

Figure 1 shows that the loans to NDFI grew steadily from the beginning of 2015, with a small kink during the first Corona lockdowns. However, at the beginning of 2025, loans saw a massive jump upward, followed by a clear acceleration in the growth rate.1 In other words, there was a spur to growth, while the commercial and industrial loans issued recorded a near-matching decrease, shown in Figure 2.

So, in the first week of 2025, a significant event, a “kink”, occurred that changed both the levels and trajectory of loans to NFDI, resulting in a notable increase in its growth rate. There was something of a mirror image of this in the C&I lending, while their growth rate after the kink seems to have remained stagnant, like it has been since the second wave of the Global Financial Crisis in mid-March 2023. During the first week of January, loans to the NFIS skyrocketed by $239 billion, while C&I lending collapsed by $135 billion. Such a simultaneous movement at the beginning of a year hints at a change in the accounting.

This structural break in the first week of January also shows up in statistical analysis. Tests indicated that both loans to non-depository financial institutions and commercial and industrial (C&I) loans are I(1) nonstationary processes, indicating that they are driven by stochastic trends. Upon testing for cointegration, the test revealed that the two series do not share the same stochastic trend process. However, when we allowed a structural break to occur in their relationship during the first week of January, the Johansen Trace Test indicated that the two series are cointegrated. That is, the two series are (stationary) linear combinations of each other, and the break is an anomaly. Also, this hints that the break is artificial (i.e., accounting-related).

In other words, tests indicate that the loans to non-depository financial institutions and commercial and industrial loans share the same stochastic trend. What does this imply?

Two (or more) series sharing a stochastic trend indicates that they are driven by the same data-generating process.2 That is, the underlying (statistical) process is the same, i.e., there’s a common denominator driving the two series. While we cannot know with 100% certainty what this is (the very essence of stochasticity), we can deduce that it relates to the business sector of the U.S. economy. This is because commercial and industrial loans are directed to businesses, mostly to the SMEs (small and medium-sized enterprises), because big corporations tend to seek funding from the capital markets. The fact that loans to NDFI series share the same underlying (stochastic) statistical structure as C&I loans series thus indicates that the former are (also) driven by developments in the U.S. business sector. This is of course no surprise, because one of the main recipients of the NFDI lending is investment funds, which managed $300 billion already in 2010 (now they manage close to $2 trillion).3 We can thus conclude that loans to NFDI and thus private credit have been an essential and growing part of business lending in the U.S. since at least 2015 (the earliest date of our data). While at first glance this may not feel like a big deal, it actually is, which we’ll detail next.

The largest U.S. banks are accumulating the risk, yet again

What we want to understand next is into which banks this risk is accumulating. There we find a categorical difference between small and large banks in what comes to loans to NFDIs and in the risk accumulating in the private credit sector. Figure 3 presents the loans to NDFIs issued by large and small U.S. commercial banks.