Weekly Forecasts 6/2026

How long for the business cycle converge and for peace to be achieved in Ukraine?

Economic indicators continue to send mixed signals regarding the future path of major economies.

When can we expect peace to be found in Ukraine?

The divergence in the leading indicators diverges.

This week, we’ll start by updating the economic indicators. They continue to convey a mixed message. Previously, we had interpreted this controversy as a sign of approaching turbulence. The analysis and forecasts we present herein enforce this view.

On the geopolitical front, we ponder the question, when do we reach peace in Ukraine? Yesterday, I noted the new “bizarre” deadline of June created, reportedly, by an ultimatum from President Trump to President Zelenskyy to hold elections and a referendum on land concessions “or else (maybe).” At the same time, Finnish president Alexander Stubb has changed his tone from aggressive to something resembling a détente (towards Russia), which indicates that the global elite have started to turn to “dialogue.” Based on these, our assessment of the prospects of peace is elevated. However, we should keep in mind that we were too optimistic also after the Anchorage summit of presidents Putin and Trump.

We end with an effort to shed light into the divergence in OECD’s leading indicators through (further) statistical modeling. Our forecasts indicate, yet again, that the global business cycle would turn down during Q2, to which Beijing would respond by ramping up the credit machine yet again.

Tuomas

Economic indicators

United States, January (December)

Richmond Fed manufacturing: -6 (-7)

Empire State manufacturing: 7.7 (-3.9)

Dallas Fed manufacturing: 11.2 (-3.2)

Kansas Fed manufacturing: 0 (0)

Manufacturing PMI: 52.4 (51.8)

Services PMI: 52.7 (52.5)

Consumer Confidence: 84.5 (94.2)

U.S. leading indicator; November (September): 97.9 (98.3)

Economic indicators paint a conflicting picture on the state of the U.S. economy. Manufacturing sector posted a clear rebound from past month continuing the slow recovery from its 2022 - 2024 slump.

However, consumer confidence published by the Conference Board collapsed below Corona lockdown depths. More damningly, the expectations index continued to sunk signaling a deepening forward-looking pessimism among the U.S. households.

The now-resumed leading indicator of the U.S. also declined in October and November. It has now continued to “nose-dive” for about four years.

The conflicting message sent by the economic indicators continues to emphasize our hypothesis that something is “brewing” in the U.S. economy. The sinking of consumer confidence indicates that household consumption can simply collapse, and the fact that expectations continue to sink indicates the likelihood of this growing. This is what our forecasting model may observe approaching, as it continues to predict an U.S. recession starting from next quarter.

Eurozone, January (December)

Manufacturing PMI: 49.5 (48.8)

Services PMI: 51.6 (52.4)

Germany ifo Business Climate: 87.6 (87.6)

While the manufacturing PMI of the Eurozone edged up, it still signaled contraction (value under 50). The ifo Business Climate index remained depressed, but did not fall further. A German economist Thomas Kolbe published an interesting piece on the recent “strength” of the German economy in Zerohedge. In it he notes that:

For December 2025, Germany’s Federal Statistics Office reported a 7.6% month-on-month jump in industrial orders. November had already provided a first boost with a rise of over 5%—right in the midst of a severe economic crisis.

But once you dissect the data and strip out large orders, a very different picture emerges. The apparent surge in orders shrinks to a mere 0.9%.

What happened? Experience shows that this comes from “Other Vehicle Manufacturing,” which jumped roughly 9.5%. This category is dominated by defense equipment. In short: the federal government’s debt-financed special fund has found its way into German military production.

This somewhat confirms what we speculated to be behind the divergence between OECD’s leading indicators of China and major four European nations in the Weekly Forecasts 42/2025, where we noted that:

The decoupling of Major-4 Europe from China all through the year is notable. While it has been just nine months, it is difficult to find another such long divergence from the data dating back to May 1992. This is likely a result of the deficit and war spending of governments, with, for example, Germany enacting major deficit spending aimed at infrastructure, security, and the military.

Our updated forecasts (see below) expect this divergence to continue to grow only for few months.

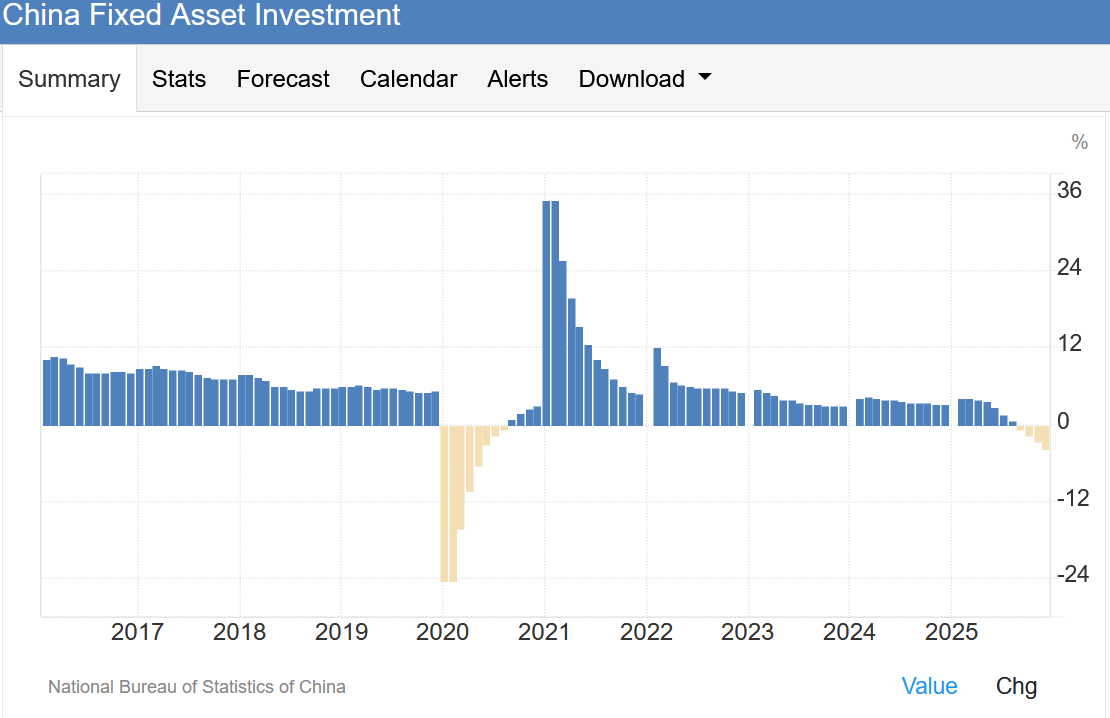

China, December (November)

Caixin (RatingDog) manufacturing PMI: 50.3 (50.1)

NBS manufacturing PMI: 49.3 (50.1)

Caixin (RatingDog) services PMI: 52.3 (52.0)

Our forecasting model anticipated an increase in the stimulus entering the Chinese economy in its last update in Weekly Forecasts 3/2026. The small uptick observed in the Caixin (RatingDog) manufacturing and services PMIs would is in line with this. However, the collapse of Fixed Asset Investments, i.e., investments on land, buildings, machinery, and technology, of China into the negative is a troubling sign for the Chinese economy going forward.

Excluding the Corona lockdowns of 2020, 2025 actually saw the first annual decline in the investments since 1989, when China experienced an economic crisis caused by runaway inflation and collapse in industrial profits (and hence production). While the collapse is now mainly driven by a drastic fall in property investments, investments in other sectors have failed to cover for it. At this point, it would be important for the services sector to start to grow rapidly through household consumption to carry the Chinese economy. However, like Tuomas noted in Exit the Dragon, Chinese consumer is maxed out. These imply both declining economy momentum from China as well as increased stimulus by Beijing to counter it. This is also what our forecasting model is anticipating.

Peace in Ukraine, when?

We have not analyzed the war in Ukraine for a while. This is because there has not been a lot to analyze, as the war has grinded on, mercilessly. In the Weekly Forecasts 2/2024 we warned that

We can now conclude that our somewhat optimistic timeline for peace did not come to be. This is mostly because Presidents Trump and Putin were unable to seize the momentum reached in Anchorage. The jury is still out for the pessimistic part (another conflict), but at current time it also looks to fail also (which would be most welcome).

As a result of this failure, our post-Anchorage assessment on the likelihood of a peace reached in the coming (three) months turned out too optimistic also. We estimated that the likelihood of a peace reached within the following three months was 85% while, for example, Grok-4 assessed that the likelihood was only 30-40%. The AI was correct on this one. To our defense, Tuomas warned on yet another failure by President Trump in Ukraine just three weeks after the Anchorage summit in The Trump failure #3, but he did not formally alter the likelihood.

What are the likelihoods by provided by us vs. Grok-4 now?